42 what is the duration of a zero coupon bond

The Macaulay Duration of a Zero-Coupon Bond in Excel - Investopedia Calculating the Macauley Duration in Excel Assume you hold a two-year zero-coupon bond with a par value of $10,000, a yield of 5%, and you want to calculate the duration in Excel. In columns A and... Zero-coupon bond - Wikipedia A zero coupon bond always has a duration equal to its maturity, and a coupon bond always has a lower duration. Strip bonds are normally available from investment dealers maturing at terms up to 30 years. For some Canadian bonds, the maturity may be over 90 years. [citation needed]

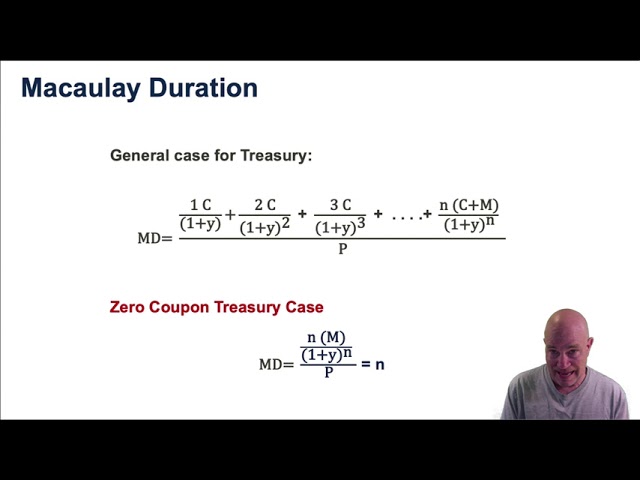

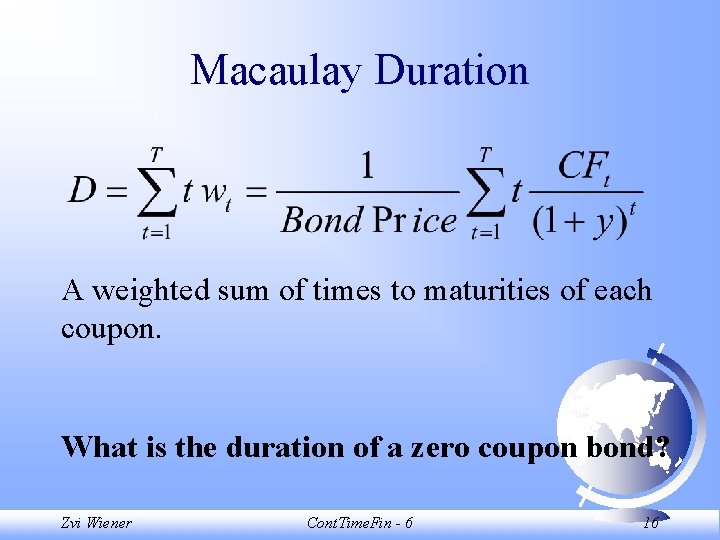

What is the duration of a bond? and How to Calculate It? The model calculates the time the present value of cash flows from a bond takes to realize. The simplified formula for Macaulay duration is as below: Macaulay Duration = Sum of PV of cash flows [PV (CF 1) + PV (CF 2) … + PV (CF n )] / Market price of the bond. See also 3 Types of Term Loans You Should Know. The cash flows of a bond consist of ...

What is the duration of a zero coupon bond

Zero Coupon Bonds: Know tax rules when such a bond is held till ... As the coupon rate of a zero coupon bond is zero per cent, people investing in such bonds don't get regular interest, but get a deep discount on face value at the time of issuance of such a bond. Zero-Coupon Bonds: Pros and Cons - Management Study Guide Zero-coupon bonds are those bonds that are sold at a deep discount to their face value. This means that these bonds do not receive any periodic interest. Instead, the investors have to invest a lump sum amount at the beginning of their investment and get paid a higher lumpsum amount at the end of their investment. What Is a Zero-Coupon Bond? Definition, Advantages, Risks Essentially, when you buy a zero, you're getting the sum total of all the interest payments upfront, rolled into that initial discounted price. For example, a zero-coupon bond with a face value of...

What is the duration of a zero coupon bond. Zero Coupon Bond Calculator - Nerd Counter For instance, the maturity period of a zero-coupon bond is 10-years, its par value is $1000, the interest rate is 5.00%. When we are calculating the bond price in Excel, suppose we use the B column of the excel sheet for entering the values where B2 is the face value, B3 is the maturity time period, B4 is the interest rate. Zero-Coupon Bond - Definition, How It Works, Formula John is looking to purchase a zero-coupon bond with a face value of $1,000 and 5 years to maturity. The interest rate on the bond is 5% compounded annually. What price will John pay for the bond today? Price of bond = $1,000 / (1+0.05) 5 = $783.53 The price that John will pay for the bond today is $783.53. Example 2: Semi-annual Compounding risk management - Calculate duration of zero coupon bond - Quantitative ... Let Pz (t, T ) be the price of a zero coupon bond at time t with maturity T and continuously compounded interest rate r. Duration = − 1 P d P d r Let A and a be two constants and x be a variable. Let F ( x) = A × e a x be a function of x. Then, the first derivative of F with respect to x, denoted by d F d x, is given by What is the duration of a zero-coupon bond that has eight years ... - Quora Answer (1 of 5): Macaulay duration is the weighted average time to cash flow, weighted by the present value of the cash flow. A zero-coupon bond only has one cash flow, so the Macaulay duration is equal to the time to cash flow, 8 years and 10 years in your question. The modified duration is the...

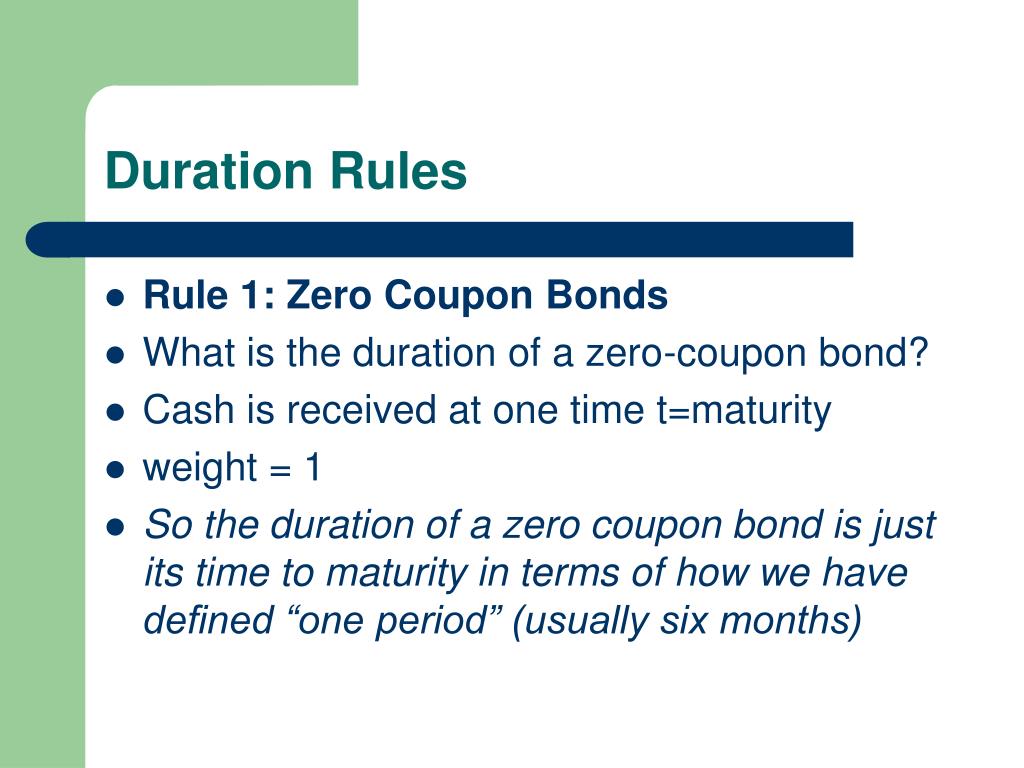

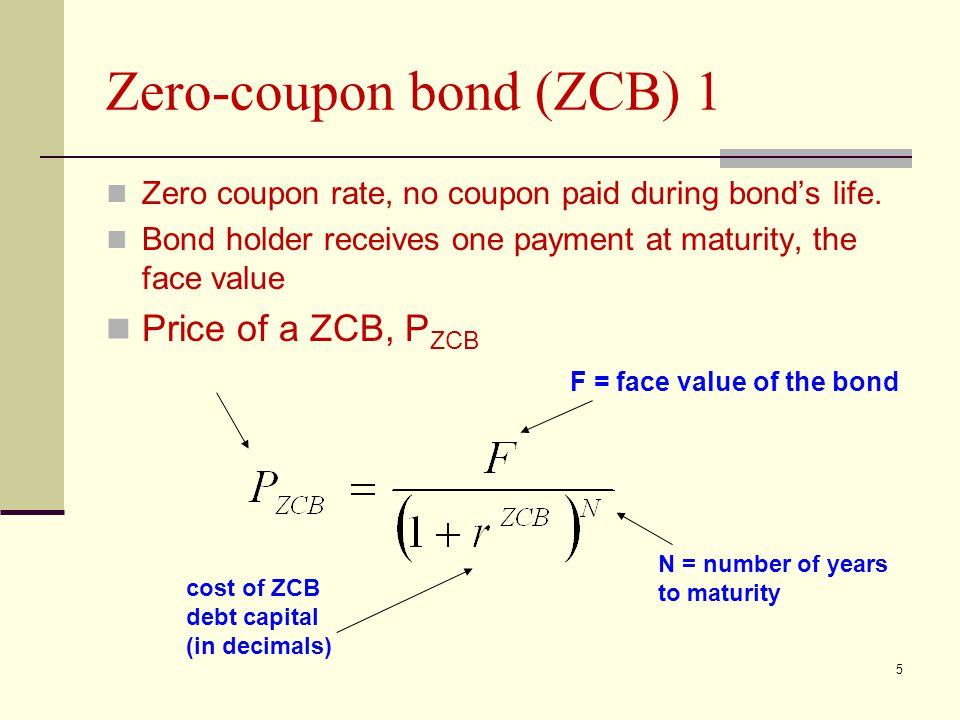

Zero Coupon Bond - (Definition, Formula, Examples, Calculations) Thus, the Present Value of Zero Coupon Bond with a Yield to maturity of 8% and maturing in 10 years is $463.19. The difference between the current price of the bond, i.e., $463.19, and its Face Value, i.e., $1000, is the amount of compound interest that will be earned over the 10-year life of the Bond. Zero Coupon Bond Calculator - What is the Market Price? - DQYDJ Duration of a bond is a length of time representing how sensitive a bond is to changes in interest rates. Since zero coupon bonds have an equal duration and maturity, interest rate changes have more effect on zero coupon bonds than regular bonds maturity at the same time. (Whether that's good or bad is up to you!) What is the duration of a zero coupon bond? - Quora The duration of a zero coupon bond is equal to its maturity. Duration is a weighted average of the maturities of all the income streams of a bond or a portfolio of bonds. Therefore if there are coupons, the duration will be less than the maturity, and if there are no coupons it will be equal to its maturity. Pete Zeman The One-Minute Guide to Zero Coupon Bonds | FINRA.org After 20 years, the issuer of the bond pays you $10,000. For this reason, zero-coupon bonds are often purchased to meet a future expense such as college costs or an anticipated expenditure in retirement. Federal agencies, municipalities, financial institutions and corporations issue zero-coupon bonds.

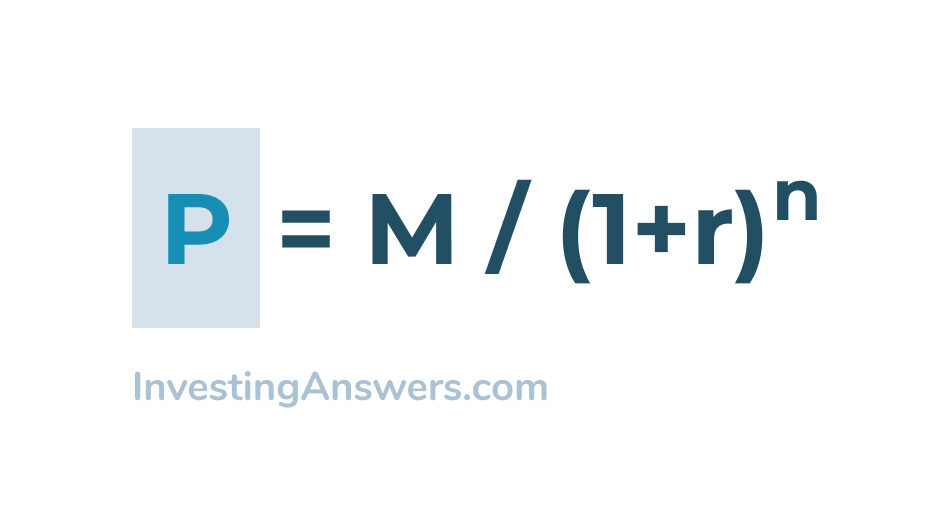

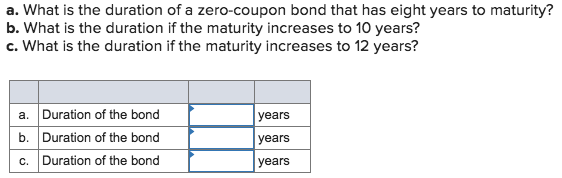

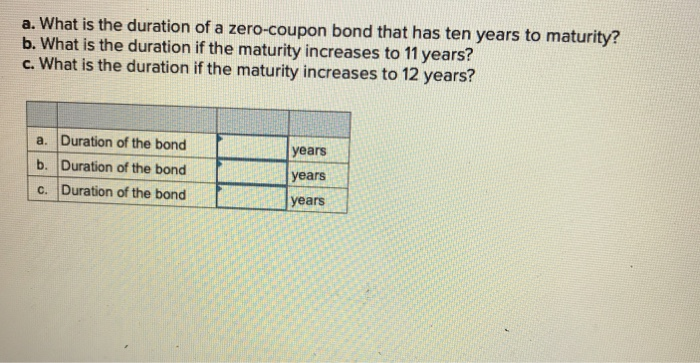

What Is a Zero-Coupon Bond? Definition, Characteristics & Example Typically, the following formula is used to calculate the sale price of a zero-coupon bond based on its face value and maturity date. Zero-Coupon Bond Price Formula Sale Price = FV / (1 + IR) N... Solved a. What is the duration of a zero-coupon bond that | Chegg.com Finance questions and answers. a. What is the duration of a zero-coupon bond that has ten years to maturity? b. What is the duration if the maturity increases to 11 years? c. What is the duration if the maturity increases to 12 years? a. Duration of the bond Duration of the bond c. Duration of the bond years years years. What is zero coupon bonds? - myITreturn Help Center Zero-coupon bond (also discount bond or deep discount bond) is a bond bought or issued at a price lower than its face value and the face value repaid at the time of maturity. It does not make periodic interest (coupon) payments. Hence the term is called as zero-coupon bond. When the bond reaches maturity, its investors receive its par (or face ... Zero Coupon Bond | Investor.gov The maturity dates on zero coupon bonds are usually long-term—many don't mature for ten, fifteen, or more years. These long-term maturity dates allow an investor to plan for a long-range goal, such as paying for a child's college education. With the deep discount, an investor can put up a small amount of money that can grow over many years.

How to Calculate PV of a Different Bond Type With Excel

A what is the duration of a zero coupon bond that has a What is the duration of a zero coupon bond that has twelve years to maturity. A what is the duration of a zero coupon bond that has. School San Diego State University; Course Title CHAP 3; Type. Homework Help. Uploaded By uwu4school. Pages 10 Ratings 86% (7) 6 out of 7 people found this document helpful;

Zero Coupon Bond Definition and Example | Investing Answers

Zero Coupon Bond Value - Formula (with Calculator) - finance formulas A 5 year zero coupon bond is issued with a face value of $100 and a rate of 6%. Looking at the formula, $100 would be F, 6% would be r, and t would be 5 years. After solving the equation, the original price or value would be $74.73. After 5 years, the bond could then be redeemed for the $100 face value.

Duration and Zero Coupon Bonds - YouTube

Zero-Coupon Bond Definition - Investopedia The maturity dates on zero-coupon bonds are usually long-term, with initial maturities of at least 10 years. These long-term maturity dates let investors plan for long-range goals, such as saving...

Duration and Convexity in Bond market

Solved 37. What is the duration of a zero-coupon bond that | Chegg.com Question: 37. What is the duration of a zero-coupon bond that has 7 years to maturity? What is the duration if the maturity increases to 10 years? If it increases to 12 years? (니 \ ( L G \) 3-7) This problem has been solved! See the answer Show transcribed image text Expert Answer 100% (1 rating)

Solved a. What is the duration of a zero-coupon bond that ...

What are Zero-Coupon Bonds? (Definition, Formula, Example, Advantages ... A zero-coupon bond is a financial instrument that does not render interest. They normally trade at high discounts, and offer full face par value, at the time of maturity. The spread between the purchase price of the bond and the price that the bondholder receives at maturity is described as the profit of the bondholder.

Zero Coupon Bond - (Definition, Formula, Examples, Calculations)

Zero-Coupon Bond: Formula and Calculator - Wall Street Prep Generally, zero-coupon bonds have maturities of around 10+ years, which is why a substantial portion of the investor base has longer-term expected holding periods.

PPT - Interest-Rate Risk II PowerPoint Presentation, free ...

What Is a Bond Coupon? - The Balance A bond's coupon refers to the amount of interest due and when it will be paid. 1 A $100,000 bond with a 5% coupon pays 5% interest. The broker takes your payment and deposits the bond into your account when you invest in a newly issued bond through a brokerage account. There it sits alongside your stocks, mutual funds, and other securities.

Bank Management 6 th edition Management Timothy W

For zero coupon bonds? Explained by FAQ Blog A zero-coupon bond doesn't pay periodic interest, but instead sells at a deep discount, paying its full face value at maturity. ... A coupon is a periodic interest received by a bondholder from the time of issuance of the bond till maturity. Zero coupon bonds, also known as discount bonds, do not pay any interest to the bondholders.

Zero-Coupon Bond - an overview | ScienceDirect Topics

Should I Invest in Zero Coupon Bonds? | The Motley Fool So for instance, a 10-year zero coupon bond priced when prevailing yields were 3% would typically get auctioned for roughly $750 per $1,000 in face value. The $250 difference would essentially...

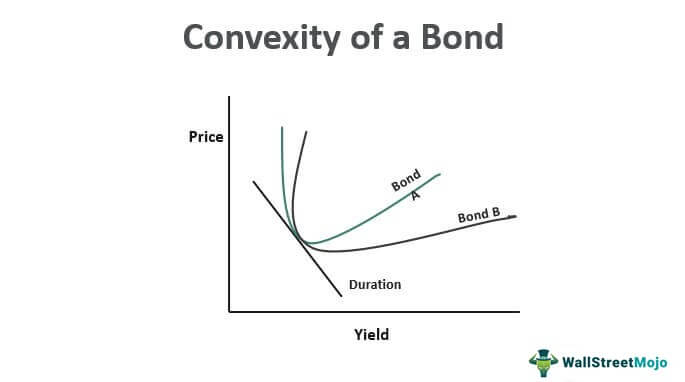

Convexity of a Bond | Formula | Duration | Calculation

What Is a Zero-Coupon Bond? | The Motley Fool Zero-coupon bonds, again, do not actually pay interest out as time passes but instead generate phantom income that is only actually paid when the bond finally matures. Most zero-coupon bonds ...

Solved a). What is the 1-year, 2-year, and 3-year spot ...

What Is a Zero-Coupon Bond? Definition, Advantages, Risks Essentially, when you buy a zero, you're getting the sum total of all the interest payments upfront, rolled into that initial discounted price. For example, a zero-coupon bond with a face value of...

Bootstrapping bonds to derive the zero curve ...

Zero-Coupon Bonds: Pros and Cons - Management Study Guide Zero-coupon bonds are those bonds that are sold at a deep discount to their face value. This means that these bonds do not receive any periodic interest. Instead, the investors have to invest a lump sum amount at the beginning of their investment and get paid a higher lumpsum amount at the end of their investment.

/DurationandConvexitytoMeasureBondRisk2-0429456c85984ad3b220cd23a760cda5.png)

Duration and Convexity to Measure Bond Risk

Zero Coupon Bonds: Know tax rules when such a bond is held till ... As the coupon rate of a zero coupon bond is zero per cent, people investing in such bonds don't get regular interest, but get a deep discount on face value at the time of issuance of such a bond.

A 12.75-year maturity zero-coupon bond selling at a yield to ...

I want to know stochastic derivation of zero coupon bond ...

WWWFinance - Bond Valuation: Campbell R. Harvey

Zero-coupon bond - PrepNuggets

Bond Economics: Primer: Par And Zero Coupon Yield Curves

4 Measuring Interest-Rate Risk: Duration

You are managing a portfolio of $1 million. Your target dura ...

Aha! Interest rates do matter.

Understanding Fixed-Income Risk and Return | IFT World

Actuarial Exam 2/FM Prep: Find Term Structure for Zero Coupon Bonds Given "Ordinary" Bond Info

Financial Engineering Interest Rates and Fixed Income Securities

PPT - 8. Measuring Interest Rate Risk-- Duration and ...

Reserve Bank of India - Database

THE DURATION OF A BOND AS A PRICE ELASTICITY AND A FULCRUM

Bond Valuation and Risk - ppt video online download

Investment Improvement: Adding Duration to the Toolbox | St ...

Zero-Coupon Bond - Definition, How It Works, Formula | Wall ...

problems 6366 involve zero coupon bonds a zero coupon bond is a bond that is sold now at a discount

Solved a. What is the duration of a zero-coupon bond that ...

Reserve Bank of India - Database

Duration model

Impossible Finance — The Perpetual Zero Coupon Bond | by ...

Bond duration - Wikipedia

:max_bytes(150000):strip_icc()/DurationandConvexitytoMeasureBondRisk2-0429456c85984ad3b220cd23a760cda5.png)

Duration and Convexity to Measure Bond Risk

Convexity of a Bond | Formula | Duration | Calculation

Zero Coupon Bonds - Financial Edge

Modified duration of zero-coupond bond (FRM practice question)

Solved a. What is the duration of a zero-coupon bond that ...

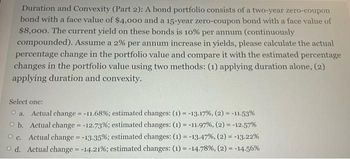

Answered: Duration and Convexity (Part 2): A bond… | bartleby

Post a Comment for "42 what is the duration of a zero coupon bond"